While the full amount of gilti is includible in the us shareholder’s income, the net gilti inclusion is reduced through a 50% deduction in tax years beginning after december 31, 2017, and before january 1, 2026 (and a 37.5% deduction in tax years beginning after december 31,. Shareholders in which or with which those tax years of foreign corporations end.

Global Intangible Low-tax Income - Working Example Executive Summary - Mksh

To be eligible for the exclusion, the cfc’s earnings must be subject to an effective foreign corporate income tax rate that is greater than 90% of the current u.s.

Gilti high tax exception pwc. While the full amount of gilti is includible in the us shareholder’s income, the net gilti inclusion is reduced through a 50% deduction in tax years beginning after december 31, 2017, and before january 1, 2026 (and a 37.5% section 163(j) business interest expense limitation. High tax exception gilti pwc. 954(b)(4) was significantly affected by the law known as the tax cuts and jobs act (tcja), p.l.

In addition, we will discuss the gilti guidance on a pwc webcast: The gilti high foreign tax exception allows a complete exclusion of gilti tested income from the federal taxable income of a u.s. Mary van leuven, j.d., ll.m.

As a result, taxpayers lobbied the u.s. Gilti as charged (3rd booking): If the cfc earns income from a foreign jurisdiction with a high tax rate, the high tax exception rules acknowledge that intangible property allocated to that.

The final gilti hightax exception from reg. Shareholder that owns a cfc. While the full amount of gilti is includible in the us shareholder’s income, the net gilti inclusion is reduced through a 50% deduction in tax years beginning after december 31, 2017, and before january 1, 2026 (and a 37.5% section 163(j) business interest expense limitation.

Shareholder that owns a cfc. On july 23, 2020, the u.s. What is the gilti high tax exception?

High tax exception gilti pwc. As discussed in a prior pwc insight, section 951a requires a us shareholder to include in income the gilti of its cfcs. Kpmg observation however, in certain cases it may still prove beneficial for a taxpayer to convert what would otherwise by tested income into subpart f income.

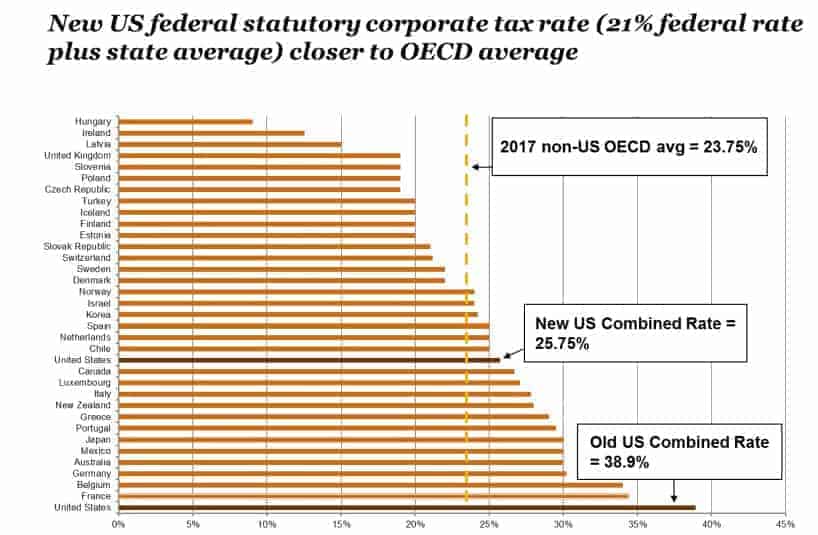

Federal corporate income tax rate. The proposed regulations provide guidance on carving out an exception from gilti gross tested income for certain income subject to ‘high tax’ in a foreign jurisdiction, as well as amending the treatment of domestic partnerships for purposes of determining a foreign corporation’s status as a cfc and Corporate income tax rate were retained.

Gilti As Charged 3rd Booking The 2020 High-tax Exception Regs Pwc

![]()

Cross-border Tax Talks Podcast - Free On The Podcast App

Gilti As Charged 3rd Booking The 2020 High-tax Exception Regs Pwc

Pwccom

Gilti As Charged Part 2 The Final Regs And High Tax Exception Pwc

Pwccom

Us Cross-border Tax Reform And The Cautionary Tale Of Gilti

Us Cross-border Tax Reform And The Cautionary Tale Of Gilti

Tax Readiness The High Tax Exception - Gilti And Subpart F Pwc

The Tax Times Final Regs Provide That Gilti High-tax Exception Is Retroactive

Us Cross-border Tax Reform And The Cautionary Tale Of Gilti

Thesuitepwccom

The High Tax Exception - Gilti And Subpart F Tax Readiness Podcast Podtail

Lwcom

Global Residence Citizenship Report 2017 Global Investor Handbook

Lwcom

Us Cross-border Tax Reform And The Cautionary Tale Of Gilti

Practical Considerations From The Hte Regulations Pwc

Pwccom

Comments

Post a Comment